Perfect Competition & Efficiency

In this section, we will see that under perfect competition, there is “productive efficiency” and “allocative efficiency”. We will also explain what these terms mean, and why they are inherent in perfect competition.

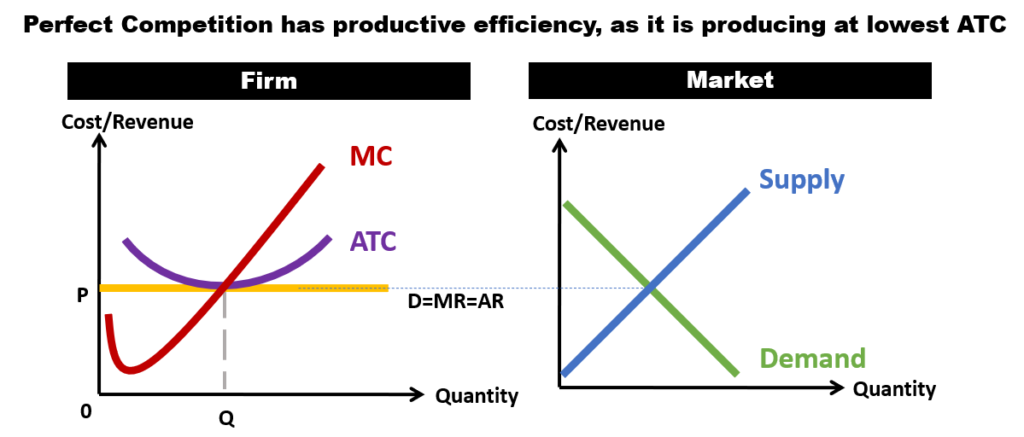

1. Productive Efficiency

Productive Efficiency means that goods are produced in the least costly way.

In the long run, pure competition forces firms to produce at the minimum average total cost of production and to charge a price that is consistent with that cost. Hence, under perfect competition, there is productive efficiency.

- From the diagram, we can see that under perfect competition the price will be set at market price P, where market demand meets market supply. This is the price in the long run scenario.

- At that price, a firm will produce at the lowest Average Total Cost (ATC). Hence, there is productive efficiency.

Taken together, productive efficiency brings about the following benefits to consumers and producers in a perfectly competitive market:

Consumers benefits, and they pay the lowest product price possible.

Firms need to use best-available (least-cost) production methods and the best combination of inputs (else it will not be efficient and hence will not survive).

However, firms will only earn normal profit in long run.

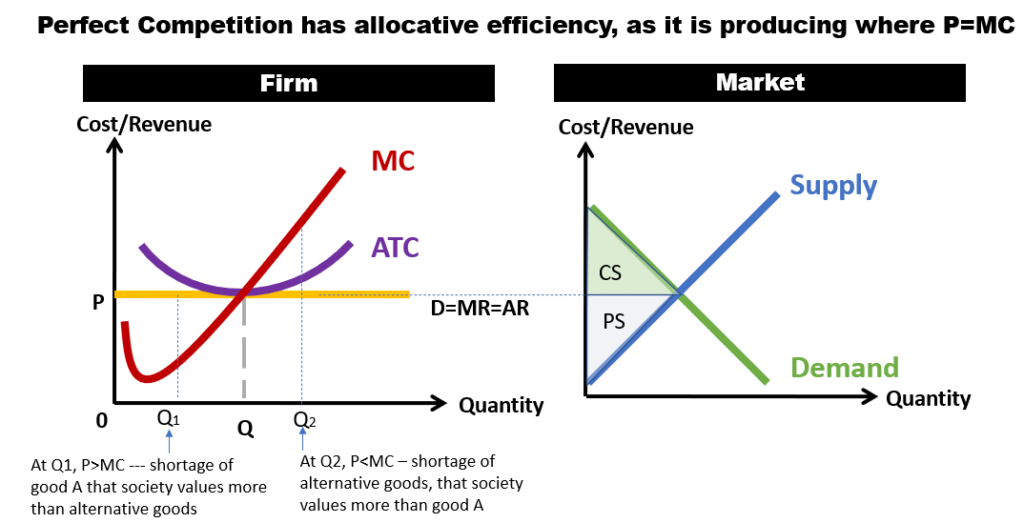

2. Allocative Efficiency

Allocative Efficiency requires that resources be apportioned among firms and industries to yield the mix of products and services to yield the mix of products and services that is most wanted by society.

Productive Efficiency alone does not ensure efficient allocation of resources. Least cost production must be used to provide society with the “right goods” (i.e. those goods that consumers want most). Essentially, in allocative efficiency there is optimal distribution of resources (e.g. capital and labour) from producers’ point of view, and optimal distribution of goods and services (from consumers’ point of view). There is no wastage as only goods and services that society wants most are produced. That is, the right type of goods and the right quantity of these goods are produced.

Additionally, if there is to be allocative efficiency, firms must produce the goods where the incremental cost of producing that additional unit (i.e. the marginal cost) must be equal to the price. Else, there will be wastage due to the misallocation of resources.

- If price is greater than the marginal cost of producing a particular good (say good A), then it means that the demand for this good must be high, compared to the amount that firms are currently producing. It also means that society values more of this good than alternative goods in the market.

- If price is lower than the marginal cost of producing a particular good (say good A), then it means that there is an excess of that good that firms are producing than what the market actually wants. Another way of saying is that market actually wants more of the alternative goods as compared to good A.

- Consumer Surplus – is the difference between the maximum prices that consumers are willing to pay for a product and the market price of that product. i.e. area between demand and market price.

- Producer Surplus — is the difference between the minimum prices that producers are wiling to accept for a product and the market price of that product. i.e. area between supply and market price.

Producers want to charge the goods for highest price possible, while consumers want to pay for these goods at the lowest possible. If we look at both producers and consumers together – that is society – then allocative efficiency means that the right goods at the right quantity are produced, and transacted at the right price where society is most happy. In summary:

- Allocative Efficiency means P = MC. This is also the point where society (i.e. both producers and consumers) benefits most.

- In other words, it is also the point where there is Maximum Consumer Surplus (CS) and Producer Surplus (PS).