Price Elasticity of Demand - looks at how big is the change in quantity over the change in price

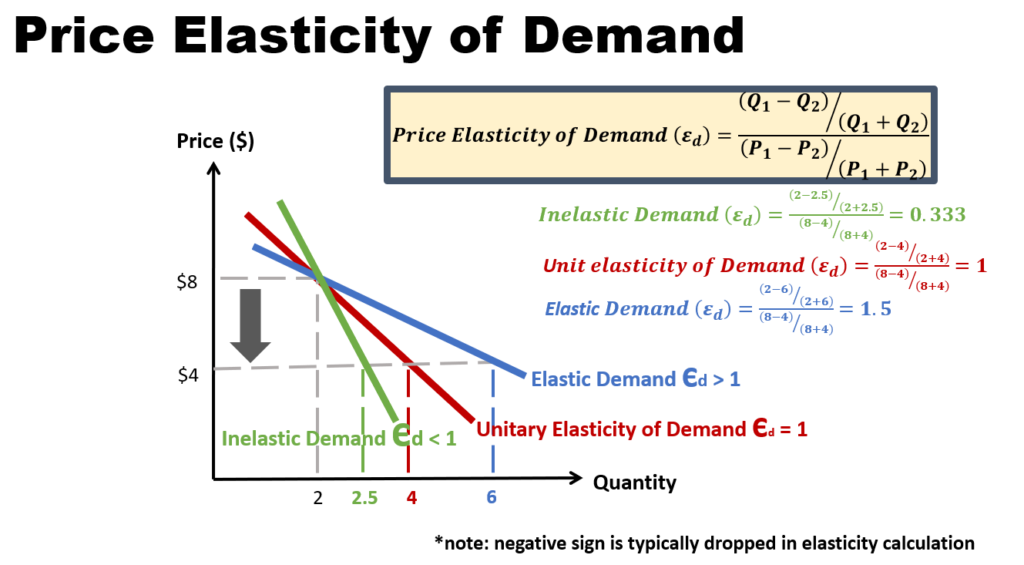

Price elasticity of demand (Ed) can be defined as the degree of responsiveness of quantity demanded to changes in price, assuming all other things remaining unchanged. The formula used to compute the price elasticity of demand is as shown in the diagram.

An elastic demand is one in which the change in quantity is larger as compared to the change in price (=> Ed>1);

while an inelastic demand is one in where the quantity change is smaller as compared to the change in price (=> Ed <1).

Factors affecting price elasticity of demand

#1 Luxuries vs Necessities

Necessities – everyone needs it all the time (e.g. essential food items, water, electricity). Hence, even if price increase, the quantity demanded will not change (i.e. will not drop) significantly.

Luxuries – these are non-essential goods that are purchased when people can afford (e.g. car). Hence if price increase, it can become too expensive for people to afford, and hence quantity demanded falls.

#2 Degree of Substitutability

If a good has a lot of substitutes (e.g. soft drink) — if price of that item increase, people will still have a lot of alternatives, and will switch to cheaper substitutes.

If a good has few substitutes (e.g. COE) – if price of that item increase, people will have little or no alternative but be forced to buy the item.

#3 Percentage of Income Spent on a Good

If percentage of income spent on good is small (e.g. Salt) – even if price increases by a huge amount, there will be little drop in quantity demanded of that good, as people can still afford it.

If percentage of income spent on good is Big (e.g. Car) – even if price increases by a small amount, there will be large drop in quantity demanded of that good, as people may have problems affording the good.

#4 Time Period

In the Short-Run — there are little possibilities for new substitutes to surface in the market. Hence consumers have no choice but to still purchase the item, even if price of that item increases.

In the Long Run — there are higher possibilities of new substitutes and alternatives for the consumers. Hence consumers can adjust their consumption patterns accordingly, if price of that item increases.